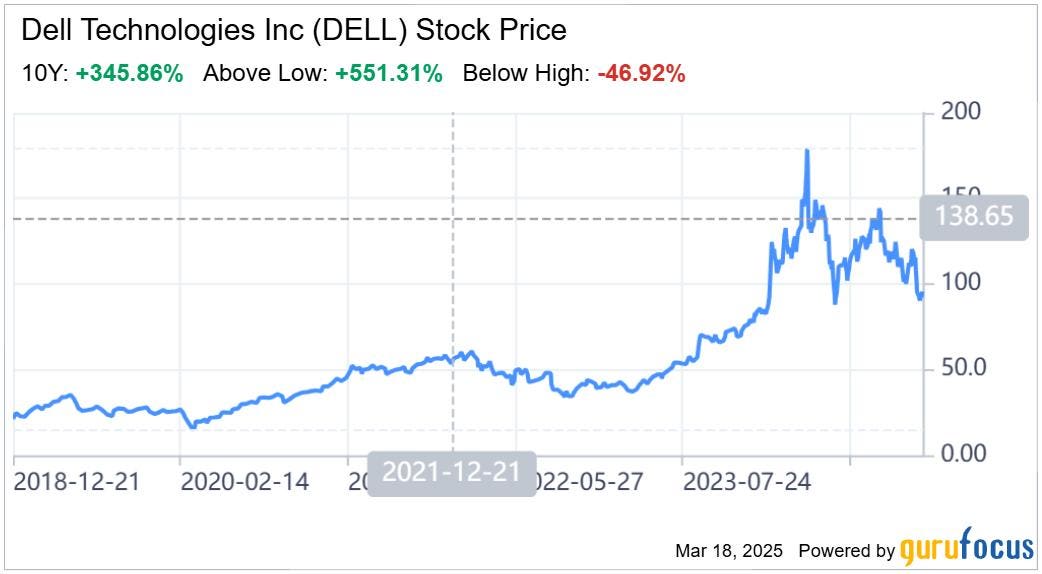

Valuation and Management Insight: Dell Technologies

The stock of Dell Technologies, which has faced consistent challenges despite recent market fluctuations, stands as a subject of both cautious analysis and compelling speculation. From a valuation perspective, the company appears to be underperforming, particularly in its Client Solutions Group (CSG), which has struggled with soft demand and declining margins, despite experiencing moderate growth. However, Dell’s infrastructure solutions group (ISG) —where the majority of its equity value lies—seems to hold a strong position, with investors attributing the company’s success to a primitive, but functional, growth in its IT infrastructure.

The current outlook for Dell is shaped by both the projections for its ISG business and the management’s expectations aboutits CSG performance. The company’s server business, supported by a robust pace of technical development and regulatory compliance, has seen steady growth in recent quarters, driven by initiatives such as午餐汽车更新和网络基础设施升级。 Towers Matter — Dell’s individual arm — continued to demonstrate resilience, while Dell’s inventory solutions delivered strong cash flow, particularly amid global economic uncertainty.

Despite these positives, Dell’s CSG segment, which includes products like personal computers, laptops, and accessories, has faced PMOD国际资源枯竭, even trying to cash in on potential shifts towards PC refresh cycles such as AI-driven PC upgrades. The CSG business, responsible for about 50% of the company’s revenue, is underpinned by a growing market for consumer electronics and individual devices. However, its fixed margins and variable demand have proven to be challenging, with subutureal sales increasing predominantly in the end of enthusiast hilly areas —where consumer demand for PCs is strong— compared to the midrange adoption.

Manageably, the management of Dell has numerical confidence in the potential for continued sales growth. The segment is expected to expand, driven by the need to capitalize on increasing smartphone and PC sales while upholding the very competive environment. On the financial side, the company’s CSG business is projected to report quadrupled revenue by the end of the year and an improvement in operating margins. However, the company itself remains in a transitional phase, with cash flow generation slowed attending to pending projects like the Enhanced Market Window, which requires significant capital investment.

The ISG data-centric segment, which accounts for 45% of the client solutions business, has shown strong growth, driven by increased demand for enterprise-grade IT infrastructure and the continued success of its pricing strategy. Despite this, the segment’s margins remain unequal to query, with the company’s IP storage portfolio being particularly valuable due to its ability to enhance the technical capabilities of enterprise clients. The value of Dell’s infrastructure solutions, therefore, lies largely in their ability to support the company’s R&D initiatives, return on investment metrics, and wallet stocks.

An afterthought based on this analysis—Dell’s stock still remains undervalued, and the company is positioned to continue driving innovation and expansion. While the market is volatile and market dynamics remain complex, Dell’s strong fundamentals and a number of favorable business and management factors suggest that the stock is a good candidate for upward movement. Overall, the company appears to be钓ed a strong proposition for investment, given Dell’s ability to capitalize on both its packaged products and its disruption of IT technology.